Dividend Hero Dillard's (DDS) is a special one

Massive annual buybacks combined with double digit dividend growth

An unexpected name for a Dividend Hero surely is department store operator Dillard’s (DDS), the $5.8 billion retailer of fashion apparel, cosmetics and home furnishings.

In fact, Dillard’s is the worst performing Dividend Hero in 2024 with a 10% negative Total Return. We will highlight why Dillard’s is a ‘special one’ and deserved a Dividend Hero selection in 2024, despite its declining revenue, low dividend yield and not much love from analysts.

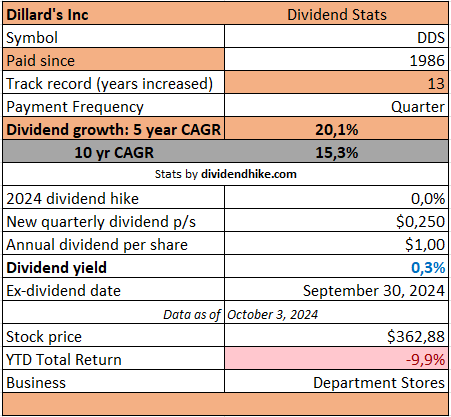

Dillard’s is known for its massive buybacks and regular double digit dividend increases with a 5 year CAGR of more than 20%. The dividend yield however is very low with just 0.3%.

Dillard’s is a well-established department store with a long history and several key strengths, such as real estate ownership and solid financial management. However, it faces significant challenges, particularly from online competitors and shifting consumer trends. The company's ability to manage inventory and maintain a loyal customer base has allowed it to stay profitable, but its limited geographic reach and slower adaptation to e-commerce represent weaknesses that could impact its long-term growth. Competition from established names like Macy's, Nordstrom, and Amazon remains a constant pressure.

The dividend history and the massive buybacks explain why Dillard’s is a Dividend Hero. But is it a good investment? Let’s take a close look at DDS and learn what we think of it.

Dillard's, Inc. (DDS) is a high-end department store chain based in Little Rock, Arkansas, that operates approximately 250 locations across the United States. Founded in 1938 by William T. Dillard, the company offers a range of products including fashion apparel, cosmetics, home furnishings, and accessories.

Dillard’s targets middle-to-upper-income customers with an emphasis on customer service and curated merchandise from premium brands. The company also operates an e-commerce platform, which has been increasingly important as retail shifts online.

History

Dillard's began as a small store in Nashville, Arkansas, and rapidly expanded through a series of acquisitions and new store openings over the decades. In the 1960s and 1970s, Dillard's capitalized on consolidation trends in retail by acquiring other regional department store chains, allowing it to grow into one of the largest department store operators in the U.S. By the late 20th century, Dillard’s had expanded its reach across the southern and western United States.

Despite facing challenges due to the rise of e-commerce and changing consumer behavior, Dillard's has managed to remain profitable, often by focusing on inventory management and real estate ownership. In fact, Dillard’s owns the majority of its retail locations, which has given it flexibility in managing operating costs, a notable advantage over some of its peers. Dillard's first offered its Class A Common Stock to the public on May 9, 1969.

Moat (Competitive Advantage)

Dillard’s does not have a wide moat in the traditional sense like companies with strong brands or near-monopolistic market positions. However, it has several competitive advantages that give it some level of protection:

Real Estate Ownership: The company owns much of its store real estate, allowing it to control operating expenses, manage lease terms, and gain asset appreciation, giving it a significant edge over competitors who lease most of their properties.

Conservative Inventory Management: Dillard's is known for maintaining tight control over its inventory, which helps minimize markdowns and protects margins. This contrasts with many retailers that face substantial discounting to move unsold merchandise.

Brand and Service Focus: The company has cultivated a loyal customer base with its focus on premium brands and personalized customer service. This niche appeal helps Dillard's compete in a crowded retail space.

Despite these advantages, Dillard's does not have a strong "moat" compared to retailers like Walmart or Amazon, which have economies of scale and technological infrastructure that create substantial barriers to entry.

Strengths

Strong Balance Sheet: Dillard’s financial health is a key strength. Its low debt levels and large real estate holdings provide significant financial flexibility. In times of economic downturns, this has allowed Dillard's to weather tough conditions better than some of its peers.

Profitability: Despite the challenges facing brick-and-mortar retailers, Dillard's has managed to stay profitable. The company’s tight control over expenses, particularly inventory, allows it to protect profit margins.

Customer Loyalty: With its focus on premium products and superior customer service, Dillard’s has built a loyal customer base, particularly among affluent shoppers.

Digital Growth: While historically slower to embrace e-commerce, Dillard’s has seen notable growth in its online sales, which is critical as more consumers shift to online shopping.

Weaknesses

Limited Geographic Reach: Dillard's operates primarily in the southern and western United States. This limited geographic footprint reduces its growth potential compared to nationwide or global competitors.

Vulnerability to Consumer Spending: As a department store chain catering to more affluent shoppers, Dillard’s is highly sensitive to economic downturns and shifts in consumer spending habits.

Competition from Online Retailers: The rise of e-commerce giants like Amazon and fast-fashion brands has challenged traditional retailers like Dillard’s. Although it has made strides in e-commerce, Dillard’s online presence still lags behind these larger players.

No Significant Technological Advantage: Dillard's lacks the technological edge and innovation seen in companies like Walmart or Target, which have heavily invested in logistics, customer analytics, and omnichannel strategies.

Competitors

Dillard's faces intense competition from a variety of retailers, both traditional department stores and online retailers. Some key competitors include:

Macy’s: Another large department store chain with a national footprint, Macy's has a larger online presence and a more extensive brand portfolio, making it a direct competitor to Dillard’s.

Nordstrom: As a higher-end department store, Nordstrom competes with Dillard's for affluent customers. Nordstrom has been particularly strong in its e-commerce growth, offering premium products and customer service.

Kohl’s: While Kohl’s targets a broader customer base with more affordable pricing, it competes with Dillard’s in the mid-market segment. Kohl’s has focused heavily on omnichannel retail and partnerships with brands like Sephora to drive traffic.

Amazon: As with all retailers, Amazon poses a serious threat to Dillard’s due to its dominance in e-commerce. Amazon's fast shipping, vast product selection, and competitive pricing appeal to consumers who might otherwise shop at traditional department stores.

Off-Price Retailers (e.g., TJ Maxx, Ross Stores): These retailers offer branded goods at discounted prices, attracting bargain-hunters who might have previously shopped at department stores like Dillard’s. They pose a competitive threat by undercutting pricing without sacrificing quality.

Dividend and Buybacks

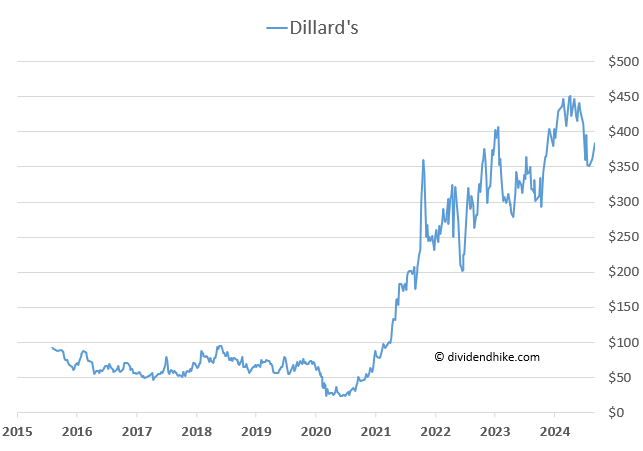

Dillard’s has done just fine with a stock price gain of more than 250% in the last decade with a huge surge right after the covid-19 pandemic lows in 2020. This year the stock is lagging with a 9.9% loss at a stock price of $362.88 as of October 3, 2024.

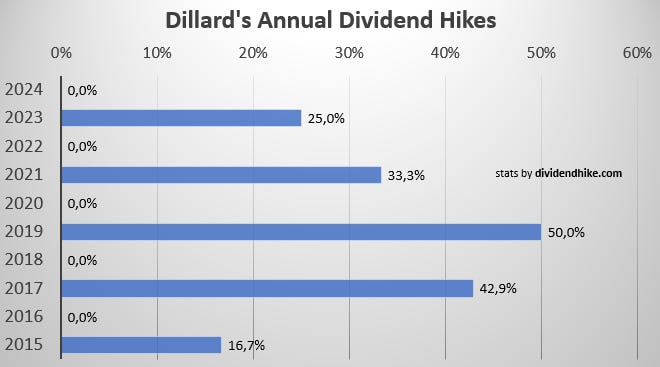

Dillard's increases its dividend every other year. Last year (2023), the dividend was raised by 25%, following a 33.3% increase in 2021. Therefore, no increase has been announced for this year, with the next one expected in 2025 as usual. However, Dillard's has consistently raised its dividend by double digits in recent years, which, given the current very low dividend yield of just 0.3%, is not particularly surprising.

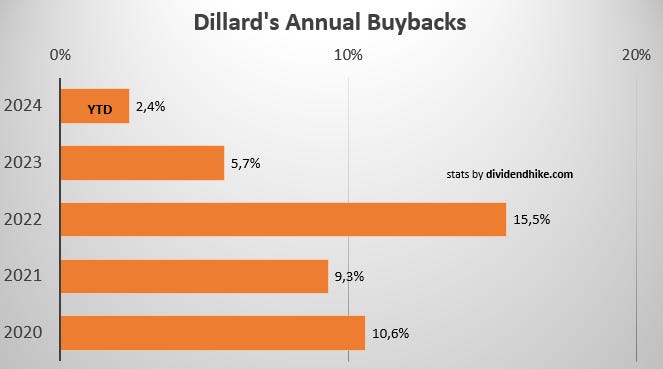

Dillard's is primarily known for its aggressive stock buybacks; according to our calculations, over the past 10 years, more than 60% of its outstanding shares have been repurchased, which is remarkable—especially considering that the dividend has also been significantly increased during this period.

In the most recent fiscal year 2024 (which ended in January), 5.7% of the outstanding shares were repurchased, following 15% in 2023, 9.3% in 2022, and nearly 11% in 2021. These are unprecedented percentages that very few publicly traded companies can achieve. Dillard's is able to do this largely due to its rock-solid balance sheet; at the end of last year, the company had a net cash position of $434 million. The dividend is unquestionably safe, as Dillard’s currently pays around $16 million in dividends annually with an estimated free cash flow of more than $700 million. Almost all of that cash is being directed toward share buybacks; given the very low payout ratio, strong dividend growth in the coming years is almost certain, especially with the company’s debt-free balance sheet.

Key Financial Metrics for Dillard’s

Forward P/E for FY 2025 (current fiscal year): 11.6

Return on Invested Capital (ROIC): 43.8% for FY 2024

EBIT Margin: 13.2% in 2024 and expected to drop to 10.2% for FY 2025

Revenue: The FY 2024 revenue declined by 3.3% to $6.48 billion and for FY 2025 (ending next January) analysts expect a 4.9% drop to $6.16 billion.

Balance sheet: Dillard’s had a net cash position of $434.9 million at the end of FY 2024, expected to rise to more than $550 million at the end of this year (this includes dividends/buybacks paid throughout the year)

Free cash flow: Dillard’s is expected to generate over $700 million in FCF this year with an annual dividend payment of $16 million, leaving lots of room for future dividend increases.

On the other hand, despite a strong balance sheet, growing dividend, and aggressive share buybacks, Dillard's is facing declining revenue, both for 2024 and the current fiscal year 2025. Additionally, there is a relatively high percentage of short sellers at over 6%, indicating that professionals are betting on a price drop for Dillard's, which is still trading right between its highest ($476.48) and lowest price ($271.59) levels of the year with a current stock price of $366.

Additionally, analysts are not very positive about Dillard's, with currently no buy recommendations. Two analysts advise a 'hold,' and two recommend 'sell' for the stock, with an average price target that is over 20% below the current level. This is a clear warning to be cautious with this stock, which has fallen 10% in 2024 for good reason. In summary, we can say that while Dillard's is a fantastic dividend and buyback stock, there are certainly fundamental challenges, given the declining revenue and negative analyst opinions.

Dividend Heroes

Last but not least: Dillard’s is one of the 2024 Dividend Heroes thanks to the combination of dividend growth and buybacks. The average Dividend Hero is gaining 26% so far in 2024, with Dillard’s being the biggest laggard right now.

Disclaimer: The information provided here is for informational purposes only and should not be considered financial advice. Investors should conduct their own research or consult with a financial advisor before making any investment decisions.