Shutterstock (SSTK): A Stock in Turmoil or a Hidden Opportunity?

A 6.5% dividend yield and 6 straight years of double digit increases

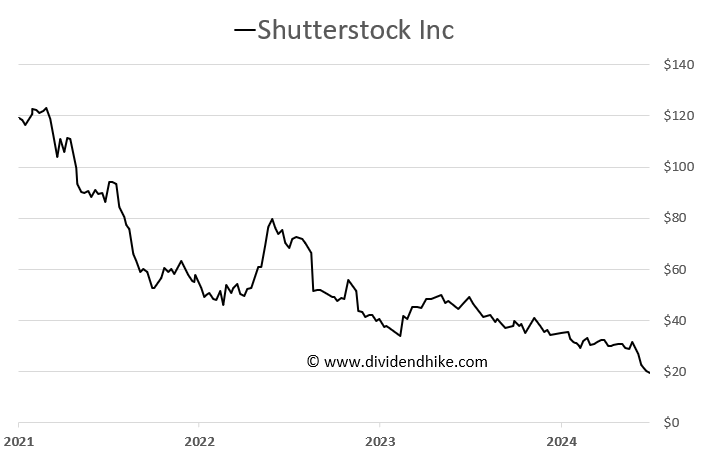

Shutterstock (SSTK) has been taking a major hit in the market this year, with its share price plummeting 35% to $19.55. This decline comes after reaching an all-time high of $120 in late 2021, marking an extreme drop. But what’s causing this sharp downturn?

While some may point to the rise of AI-generated imagery, which has made it easier for individuals to create their own images, Shutterstock's troubles seem to run deeper. The company, which once dominated the stock photo industry, now faces a market where many others are offering similar services at a lower cost, or even for free.

Shutterstock is a global provider of stock photography, videos, music, and editing tools for creative professionals and businesses. It offers a vast digital library with millions of royalty-free assets, allowing users to license content for various projects.

History

Shutterstock was founded in 2003 by Jon Oringer, who initially uploaded 30,000 of his own photographs to create a subscription-based stock image platform. The company rapidly grew, expanding into video, music, and AI-driven creative tools. It went public in 2012 on the New York Stock Exchange (NYSE: SSTK) and has since acquired several companies, including Bigstock, Flashstock, and TurboSquid (a 3D content platform).

Competitors

Shutterstock faces competition from several major stock media companies, including:

Adobe Stock – Integrated with Adobe Creative Cloud, offering seamless access for designers.

Getty Images – A premium stock image provider known for high-quality editorial and commercial content.

iStock – A budget-friendly subsidiary of Getty Images.

Depositphotos – A growing stock photo and video platform.

123RF – Offers royalty-free images, vectors, and audio.

Another partially similar company currently in trouble is Adobe Systems, which dropped 14% yesterday after its earnings report and outlook, with analysts expressing dissatisfaction over the company's AI monetization, particularly through products like Photoshop and Adobe Stock.

Fundamentals and dividend

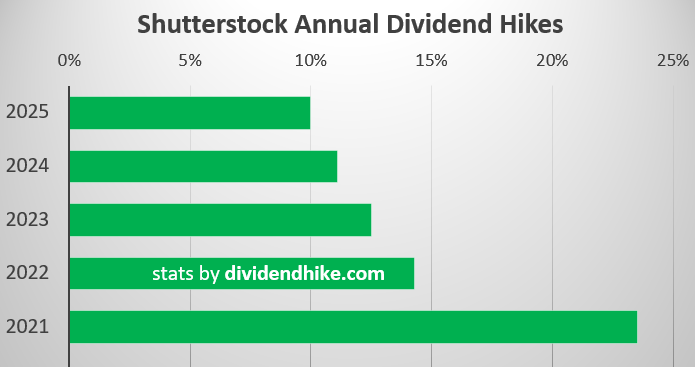

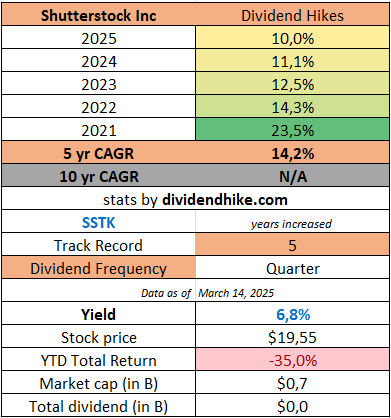

Despite this tough landscape, there are some interesting numbers that stand out. Shutterstock’s P/E ratio is currently just 4, a stark contrast to the typical valuation for companies of its size. Its dividend yield stands at 6.5%, which, for many investors, might seem like an appealing opportunity. The company raised its dividend by 10% this year, continuing a trend of double-digit dividend increases for the fifth consecutive year since its first payout in 2020.

But are these figures signaling a "value trap" or a massive buying opportunity?

Let’s take a closer look at the facts:

Revenue Growth: Shutterstock's revenue has been growing year on year, with a 6.9% increase in FY 2024, reaching $935 million. Analysts expect this growth to continue, with 11.2% growth forecasted in 2025, reaching $1.04 billion, which would mark a new record for the company.

Share Repurchases: In addition to its dividend, Shutterstock is also repurchasing its own shares, which could provide additional support to the stock price in the long run.

Minimal Debt: Shutterstock is nearly debt-free, with an estimated net debt of less than $100 million expected by the end of 2025 based on analyst estimates.

However, there are concerns to consider:

Negative Free Cash Flow: For the first time in years, Shutterstock reported negative free cash flow (-$0.41 per share) for 2024. This marks a significant decline from its peak of $5.04 per share in 2021. While analysts expect a rebound in 2025, projecting a free cash flow of $2.50 per share, this remains a key metric to watch. If free cash flow continues to decrease, the sustainability of the current dividend could be at risk.

Return on Invested Capital (ROIC): In 2024, Shutterstock’s ROIC was 10.2%, with an EBIT margin of 10%. While these are positive indicators of the company’s operational efficiency, they are not enough to fully offset the negative cash flow and valuation concerns.

What are analysts saying? Currently, 4 analysts are following Shutterstock’s stock. There’s 1 buy recommendation and 3 holds, with no sell recommendations. This suggests that, while many analysts are cautious, they still see potential in the company.

In summary, Shutterstock seems to be caught in a dilemma. On one hand, its low valuation, high dividend yield, consistent revenue growth, and debt-free status make it an attractive candidate for investors seeking value. On the other hand, the negative free cash flow, ongoing challenges with AI, and overall market sentiment might signal that this stock is best avoided for now.

Is Shutterstock a hidden gem or a stock you should steer clear of? Let us know your thoughts and opinions in the comments below!

Disclaimer: The information provided here is for informational purposes only and should not be considered financial advice. Investors should conduct their own research or consult with a financial advisor before making any investment decisions.

Thanks everybody for their votes on our Shutterstock poll so far!!